The commoditisation of trade receivables in a digital era

The digitalisation of trade and the use of credit insurance and capital markets techniques within trade finance make it an attractive asset class for investors, helping narrow the trade finance gap. AIG’s Ana Velandia Evan, Global Head of Trade Finance, and Benjamin Tolédano, Global Head of Structured Trade Finance, share their views.

We are living in an increasingly uncertain world where companies and financial institutions face new challenges which add complexity to how they manage liquidity, counterparty risk, capital efficiency and returns on investments. Addressing these challenges through incentivising collaboration, accelerating the development of innovative solutions, encouraging the improvement of existing mechanisms available in the market, or simply providing a different perspective on new needs can lead to further opportunities for market players.

Trade finance is one area of finance that is evolving quickly in this environment. The industry is going through a digitalisation journey and is attracting global interest and investment. This is due to the attractive risk profile and the self-liquidating nature of trade finance assets, the support these instruments provide to the real economy and their resilience during turbulent times. The use of sophisticated structures is also adding to the resilience of the industry and allowing financers to support more complex types of risk.

Addressing the trade finance gap

We must acknowledge that the difference between the demand for trade finance and those who are able to access it has led to the trade finance gap reaching a high of US$1.7tn in 2020 according to the Asian Development Bank (ADB).1 The gap widened during the pandemic due to economic uncertainties and supply chain challenges, particularly impacting small and medium-sized enterprises. In order to close this gap, sophisticated solutions are required to provide comfort for investors to deploy capital to those who are often unable to access their required financing. This would include well-structured transactions with the use of credit insurance to provide sufficient risk mitigation.

Within the trade finance industry, one solution for the financing gap that is being used more often as an alternative to traditional structures of open account programmes is the securitisation of trade receivables. While this may not be a new concept, it has been evolving rapidly, supported by new technology, distribution channels and credit insurance providers. This has led to investors, who were typically more familiar with capital markets transactions, entering the trade finance space. The emergence of these new players is supporting a more open industry. At the same time, the structured solutions currently used in trade finance are helping traditional lenders to manage capital and risk more efficiently while supporting the growth of the programme they have offered to their clients.

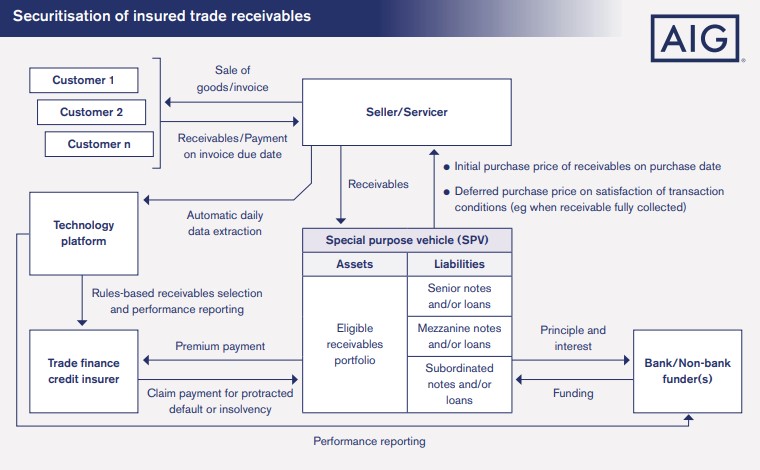

In a typical trade receivable securitisation structure, the seller sells to its customer (the ‘buyers’) on credit, which creates a working capital requirement for the seller. This can be financed through the sale of the receivables, created between seller and buyers, to a special purpose vehicle (SPV) on a revolving basis, for a set period (subject to early termination on the occurrence of certain triggers). The SPV is financed by issuing notes or borrowing loans from bank or non-bank funders who are repaid by the SPV utilising the proceeds from the buyers’ payments. Receivable securitisation transactions are often set up with a medium or long-term view (for example, three to five years), with the possibility for periodic extension(s). This enables the seller to have access to a stable and committed source of capital and amortise the setup costs of the transaction over several years.

Other trade finance structures are simpler and do not use an SPV. For example, the seller may sell its receivables directly to a bank or non-bank funder or borrow a loan from the funder, secured by the receivables portfolio.

The credit quality of these transactions can be enhanced by offering credit insurance to the SPV covering the non-payment and insolvency risk of the buyers, subject to certain pre-set eligibility criteria being met in respect of the receivables and the buyers. Credit insurance can support the transaction in obtaining a credit rating from an international rating agency. This would potentially allow larger concentrations on certain buyers compared to uninsured options, and gain access to the asset-backed securities market by appealing to investors who may not have the expertise or the mandate to invest in traditional trade finance products. In addition, the insurance policy wording can be Basel III/ CRR-friendly, which could translate to a better return on capital for the participant banks and more competitive funding terms and cost savings for the seller compared with either unsecured or secured but uninsured financing.

The role of technology

Data assessment is essential, and technology plays an important role in these transactions, facilitating real-time receivables performance reporting to all interested parties. This leads to more informed decisions and verifies that the receivables offered for purchase comply with the agreed eligibility criteria. Ultimately, it provides more certainty to all parties involved in the transaction.

Distribution of trade finance assets has evolved over the years. Nowadays, tech platforms are expected to play a key role in the commoditisation of receivable securitisation transactions, not only through the distribution of assets, but also by streamlining the end-to-end process among all parties in a digital environment.

Pulling together all the elements of the structure and technology can create a more attractive investment and opportunity for investors to diversify into a new asset class of trade receivables, but within a structure they understand.

The transformation of the trade finance industry is in its infancy with exciting times ahead, supported by new participants joining with fresh ideas. This will help drive the modernisation and technification of the industry, contributing to the reduction of the trade finance gap.

------------------------------------------------------------------------------------------------------

Reference

1. https://www.adb.org/news/global-trade-finance-gap-widened-17-trillion-2020

This article first appeared in GTR’s Supply Chain Finance issue, August 2022.

For more information about the wider team and AIG’s capabilities in this area please contact Meera Saunders, Head of Strategy and Operations, Trade Finance at meera.saunders@aig.com

This article may contain third party content or links to third party websites. These content and links are provided solely for your convenience and information. AIG has no control over, does not assume any liability or responsibility for and does not make any warranties or representations as to, any third party content or websites, including but not limited to, the accuracy, subject matter, quality or timeliness.

##

American International Group, Inc. (AIG) is a leading global insurance organization. AIG member companies provide a wide range of property casualty insurance, life insurance, retirement solutions and other financial services to customers in approximately 70 countries and jurisdictions. These diverse offerings include products and services that help businesses and individuals protect their assets, manage risks and provide for retirement security. AIG common stock is listed on the New York Stock Exchange.

Additional information about AIG can be found at www.aig.com | YouTube: www.youtube.com/aig | Twitter: @AIGinsurance www.twitter.com/AIGinsurance | LinkedIn: www.linkedin.com/company/aig. These references with additional information about AIG have been provided as a convenience, and the information contained on such websites is not incorporated by reference herein.

AIG is the marketing name for the worldwide property-casualty, life and retirement and general insurance operations of American International Group, Inc. For additional information, please visit our website at www.aig.com. All products and services are written or provided by subsidiaries or affiliates of American International Group, Inc. Products or services may not be available in all countries and jurisdictions, and coverage is subject to underwriting requirements and actual policy language. Non-insurance products and services may be provided by independent third parties. Certain property-casualty coverages may be provided by a surplus lines insurer. Surplus lines insurers do not generally participate in state guaranty funds, and insureds are therefore not protected by such funds.